Alternative Mortgage Strategies for Real Estate Investors (And How to Choose the Right One)

Real Estate CoachingBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

When it comes to financing investment properties, investors tend to think their options are either cash, a conventional loan, or hard money. And while those are all valid approaches, they only represent a small portion of the options that are actually available to investors.

While there are many options available, investors too often choose a loan based on the deal directly in front of them without understanding how that decision fits into their broader strategy. But financing isn’t just a transaction in the process; it’s a key factor that can either support or limit how the investment performs over time.

The right loan isn’t one that gets the deal done the fastest, but one that supports your goals and portfolio strategy while positioning you for what’s next.

That’s why, in this article, we’re going to look at how to think more strategically about alternative financing, talk about some options beyond the standard choices, and walk through how we encourage clients to make longer-term financing decisions that work for their investment plan.

Start with Planning, Not the Loan

Before getting started with specific loan options, it’s important to take a step back and get clear on what you’re actually looking to accomplish with a real estate investment.

Financing decisions shouldn’t be made in a vacuum; they should support the broader plan for how you want your portfolio to grow over time. That starts with a few common questions:

- Are you planning to buy and hold, or is this a flip?

- Is this your first property, or are you actively scaling a portfolio?

- Are you prioritizing cash flow today, or longer-term appreciation?

Depending on your answers to these questions, the type of financing that makes sense for you could be drastically different.

When real estate investors make decisions with only the current deal in mind, it’s easy to choose a loan that may work today and create friction later. This could limit your ability to qualify for future property mortgages, reduce cash flow, or introduce unnecessary risk.

Taking a long-term perspective helps avoid that, because ultimately, financing is about positioning yourself for what’s next just as much as it is about getting into a current property.

Working with a Mortgage Broker

Once you’ve gotten really clear with your strategy and the business plan for your real estate business, the next step is to find the right financing to support it. That’s where working with a good mortgage broker can make a big difference.

Once you’ve gotten really clear with your strategy and the business plan for your real estate business, the next step is to find the right financing to support it. That’s where working with a good mortgage broker can make a big difference.

Unlike a traditional lender that offers a fixed set of products, a broker works across multiple lenders, effectively shopping the market on your behalf and matching your specific situation to the right loan options.

Every borrower is different; some have a solid W2 income and clean financial history, others may be self-employed, managing multiple properties, or have more complex financial profiles. A single lender may not have the right solution for every scenario, so having a broker with access to a broader range of options can offer flexibility to real estate investors.

Instead of trying to force your situation into a limited set of options, a broker allows you to approach financing more strategically.

The Role of Cash Flow

While looking at financing options, it’s important for investors to stay grounded in what actually drives long-term growth in a real estate portfolio - cash flow.

Consistent, positive cash flow isn’t just a measure of whether a property is performing. It’s often what drives your ability to acquire the next one. It creates flexibility, helps build reserves, and allows you to continue investing without relying solely on external capital.

For many real estate investors, the traditional approach has been to tap into equity through refinancing and use the appreciation to fund future purchases (BRRRR). In a higher interest rate environment, however, that strategy has become more difficult to execute without negatively impacting cash flow.

The structure of your loan directly affects your monthly payment, which in turn affects how a portfolio supports or limits your growth ability.

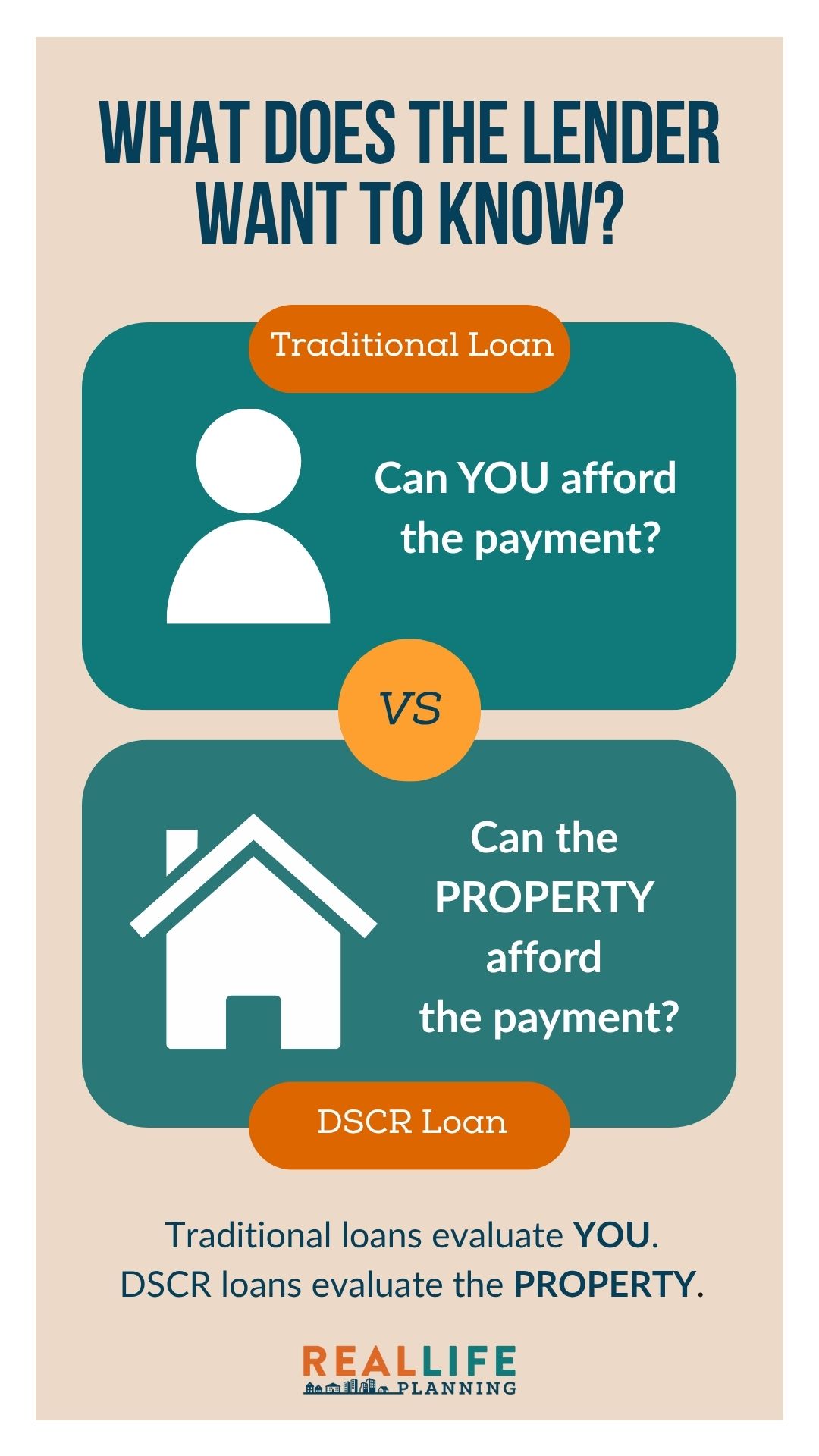

Understanding DSCR Loans

Understanding DSCR Loans

One of the most commonly used alternative financing options for real estate investors is the Debt Service Coverage Ratio (DSCR) loan. Unlike traditional loans, which focus heavily on your personal income and debt-to-income ratio, a DSCR loan is based primarily on the property itself.

The lender looks at whether the property’s expected rental income is sufficient to cover the loan payment, along with taxes and insurance. If the numbers support the debt, the loan can often be approved quickly, regardless of your personal income situation.

Key features of these loans include:

- No traditional debt-to-income requirements

- Approval based on projected rental income from an appraisal

- Typically a faster and more streamlined approval process

When to Use a DSCR Loan

Because of how they’re structured, DSCR loans can be especially valuable for investors who are actively scaling a portfolio. They can also be an option for investors who are self-employed or have complex income that doesn’t fit traditional underwriting.

DSCR loans offer a level of flexibility that’s often difficult to find with conventional financing. With that said, it’s important to understand what these loans don’t account for.

While the lender is evaluating whether the rent covers the loan payment, they’re not factoring in many of the real-world expenses that impact actual performance, such as vacancy, maintenance, property management, and other operating expenses.

That means a property can qualify for financing and still not be a good investment option.

Alternative Financing Options with Non-Traditional Income

One of the biggest challenges for many real estate investors is how income is evaluated.

Traditional lending is built around W2 income, where there are steady paychecks, consistent documentation, and clearly defined earnings. But for many investors, that framework doesn’t reflect their situation.

Self-employed income can fluctuate. Business owners have write-offs that reduce their taxable income, which can reduce the amount of income that may qualify under many traditional options. And experienced real estate investors may have strong cash flow and assets, but not the kind of income that fits neatly into a conventional underwriting model.

That’s where alternative financing options can be helpful for investors who need a different level of flexibility.

Bank Statement Loans

Bank statement loans are one of the most commonly used alternatives. Instead of relying on tax returns, lenders evaluate income based on deposits over a set period of time (typically 12 months).

This can provide a more accurate picture of self-employed individuals or business owners whose reported income may not fully reflect their real cash flow.

No-Doc Loans

No-doc (or low-documentation) loans are an option where minimal income verification is required. These programs tend to focus more heavily on credit profile and available assets, making them a potential option for borrowers with healthy financial positions but less traditional income documentation.

Asset-Based Loans

Asset-based loans are designed for borrowers whose financial position is tied more to what they own than what they earn. In these cases, lenders evaluate the borrower’s net worth and available assets to determine eligibility.

This can be particularly useful for retirees or high-net-worth investors who may not have a consistent income but have substantial reserves.

Financing Can Change as You Scale

As your real estate portfolio grows, your financial profile often changes with it. So does how lenders evaluate you.

Many investors start with W2 income, where earnings are relatively straightforward and easy to document. Over time, however, as you become more focused on real estate or transition into self-employment, your income may look very different on paper.

This is where challenges may arise for investors. Even if you’re generating strong cash flow or bringing in significant revenue, what most lenders care about is the income that shows up on your tax returns. And if you’re actively using deductions to reduce your tax liability (as many investors do), your reported income may be much lower than your actual earnings.

In other words, high income doesn’t always translate cleanly into usable income for traditional lending. This can create a disconnect that can limit your ability to qualify for conventional financing, even as your portfolio becomes more successful.

How Joint Ventures Can Affect Your Strategy

As investors look to grow, partnering with others can become part of the strategy. That might mean buying with a spouse, teaming up with a friend, or working with another investor to access larger opportunities.

As investors look to grow, partnering with others can become part of the strategy. That might mean buying with a spouse, teaming up with a friend, or working with another investor to access larger opportunities.

And while partnerships can come with meaningful benefits like shared capital, shared risk, and increased capacity, they also introduce another layer of complexity.

The most common challenges tend to come from incomplete planning rather than the deal itself. Differences in goals, disagreements about when to sell, or uneven contributions can create friction over time. Without a clear structure in place, those issues can become difficult to resolve.

That’s why we often encourage clients to approach any partnership as a business arrangement from the very beginning. That includes putting a formal agreement in place, clearly defining roles and responsibilities, and outlining how important decisions will be made.

Just as importantly, it means thinking through what happens if one partner wants to exit and the other doesn’t. While these conversations may seem premature, it’s essential to have all of this figured out before moving forward with a deal.

Think Like a Business Owner, Not a Personal Home Buyer

If you’re a long-term real estate investor or scaling a real estate portfolio, it’s important to look at your investing as a business. How you approach decision-making has to reflect this mindset.

Each property isn’t a transaction, but a part of a larger decision that comes with decisions about operations, time, and risk. This includes questions like:

- Will you manage the property yourself, or hire a property manager?

- Are you investing in markets you understand, or expanding into unfamiliar areas?

- How involved do you want to be in the day-to-day management of your properties?

These decisions all have a direct impact on how your portfolio performs. They can influence your time commitment, your exposure to risk, and ultimately your profitability.

A hands-on approach may improve margins but take time away from other priorities. A more passive approach may free up your time but introduce added costs. Neither approach is necessarily right or wrong, it just needs to be intentional.

Prepare Before Talking to A Lender

One of the most common mistakes investors make is waiting until it is too late in the process to involve a lender.

The first conversation often happens after a property is already chosen, or even once an offer is being prepared. At that point, decisions are rushed, options are limited, and there’s not much time to fully think through the overall strategy.

Speaking with a lender before you actively begin looking at properties, on the other hand, gives you the opportunity to fully understand your options and what a realistic budget may look like. It also allows time for better questions.

Instead of trying to make decisions under pressure, work with a lender earlier in the process. This offers you more time to evaluate tradeoffs, work through assumptions, and make adjustments before you commit to a deal.

Run the Numbers Before You Make a Decision

When looking at an investment property, it’s easy to anchor on the purchase price, but two properties with the same price tag can produce very different outcomes.

When looking at an investment property, it’s easy to anchor on the purchase price, but two properties with the same price tag can produce very different outcomes.

That’s because what ultimately matters isn’t the price, but the monthly payment and how that translates into real cash flow.

Why Monthly Payment Matters

Your monthly payment is affected by variables like property taxes, insurance costs, interest rates, and loan structure. Even small differences in these inputs can significantly change the overall cost of holding the property.

That cost directly determines whether a deal produces positive cash flow or becomes difficult to sustain over time.

This is where a deeper analysis becomes necessary. While a lender may approve a loan based on a certain set of criteria, that doesn’t mean the investment makes sense for you. Lenders are looking for whether the loan can be supported, not whether it’s the best fit for your financial goals.

That part is your responsibility. A full analysis should include:

- All operating expenses (not just principal, interest, taxes, and insurance)

- Realistic cash flow projections

- Risk factors, including vacancy and unexpected costs

The Right Loan Supports Your Long-Term Real Estate Strategy

Financing is often treated as a step in the process or something you figure out once you’ve found a property. In reality, it plays a much bigger role than that.

The way you finance your investments influences your cash flow, your ability to scale, and how your portfolio performs over time. It’s not just a tool to get a deal done, but a strategy that should fit where you’re trying to go.

That’s why we encourage clients to think beyond the immediate transaction, consider how options fit into their broader plan, and build a team that can help them navigate options and answer questions along the way.

Ultimately, the right loan isn’t always the one that’s the fastest or easiest to secure. The right option for you is the one that supports your long-term portfolio strategy and sets you up for what comes next.

If you’re looking through your options for your next investment, it’s helpful to have a conversation early with a lender, financial planner, and/or Realtor®. That way, you can build a financing approach that supports your goals before you ever make an offer.

If you’re a real estate investor looking to scale your portfolio or get started in the space, check out more from the Real Life Blog for more insights on real estate investing from our real estate financial planning team.

This blog is for general financial education purposes. Information contained in this blog should not be construed as financial, tax, real estate, legal, or investment advice. For educational purposes, blog posts may contain links to other websites which are not under the control or and are not maintained by Real Life Planning. Real Life Planning has provided those links for your convenience but does not necessarily endorse all the material on those sites. Please consult your financial, real estate, legal, or tax advisor for advice specific to your situation.