Ask These 6 Questions Before Borrowing a Hard Money Loan

Real Estate CoachingBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

| 🏠 | how private lending is different from traditional mortgage lending |

| 🏠 | common hard money loan terms |

| 🏠 | situations where real estate investors might use a hard money loan |

| 🏠 | How to manage the risks of borrowing hard money |

Hard money loans are a quick, short-term financing option for real estate investors. These hard money loans, synonymous with private lending, are loans where lending comes not from a bank or a savings and loan, but from a private individual or a group of individuals who are lending in private transactions.

Hard money loans are very common in real estate investing, especially for properties that might not otherwise qualify for traditional bank lending, or for borrowers who might not qualify for traditional bank lending.

Private lending typically happens in circumstances like “renovate and sell” transactions (or a fix-and-flip), a “renovate and rent” transaction where either the property or the borrower would not qualify for a traditional loan, or in new construction projects. These can be in the form of owner-lending, cash-out refinancing, or private mortgage loans.

How Does Private Lending Compare to Traditional Bank Loans?

The loan terms in a private lending transaction typically have some differences from traditional bank loans.

The loan terms in a private lending transaction typically have some differences from traditional bank loans.

The first thing to know is that hard money loan rates are typically considerably higher than a traditional lender. Unlike a conforming loan or a conventional loan, these loans are not sold or securitized after the loan closing process. This means that interest rates are much higher, so that the lender makes a return on the loan.

A gold star borrower, like an experienced flipper with many projects in their history and a good record of delivery, might pay a minimum of 10-11% in this interest rate environment. Rates for inexperienced borrowers might be as much as 16-18%, not too dissimilar from some credit card rates of interest.

What Are the Typical Terms of a Hard Money Loan?

Private lending, or hard money, often has an origination fee. Typically, that's going to be 3-5% of the loan balance — plus regular closing costs for the loan, like getting an appraisal, if necessary.

These loans are typically short-term loans, meaning they could be as short as 3-6 months or as long as 18+ months. Generally, we’re looking at a term of 16-18 months for a hard money loan. Hard money loans are often interest-only during the initial period, and then they may be later refinanced with a conventional loan.

money loans are often interest-only during the initial period, and then they may be later refinanced with a conventional loan.

A private loan often has a prepayment penalty, which helps the hard money lender — usually a private individual or a fund of private investors — lock in that rate of return for the loan period. One helpful aspect of hard money loans, however, is that they typically don’t take long to close. An investor could close one of these loans in as little as 1-3 weeks.

Loan amounts are typically 80-90% of the project cost, or 60-70% of the after-repair value (a conservative estimate of what the property will be worth after the repairs and renovations are made).

Hard money loans are typically more difficult to get than a 30 or 15-year mortgage from a bank. In comparison, the underwriting process tends to be much quicker, the interest costs are higher, and it's more flexible to meet different kinds of situations.

When Would Someone Use a Hard Money Loan?

Hard money, or private money, is often used when the property or the borrower wouldn't meet the conventional underwriting standards.

For example, in the case of a flipper, they might buy a property that needs a lot of renovations or structural work. Consequently, a bank likely wouldn’t appraise that property very highly, or might not lend on it at all.

For example, in the case of a flipper, they might buy a property that needs a lot of renovations or structural work. Consequently, a bank likely wouldn’t appraise that property very highly, or might not lend on it at all.

A flipper may also borrow to fund their construction project, which is not something that a regular bank would typically lend on.

An investor or flipper would opt for a hard money loan when they can’t finance that project through a bank, when the timeline is really fast, or if, as the borrower, they don't have enough capacity to borrow from a traditional lender (in terms of their debt-to-income ratio, for example).

There are underwriting standards in hard money loans, but because it's a private transaction, the lender can be a little bit more flexible than in other scenarios. In some cases, they'll charge more to cover the risks of lending money in these situations.

Risk Management for Hard Money Borrowing

There are many risks that you want to consider when thinking about hard money borrowing.

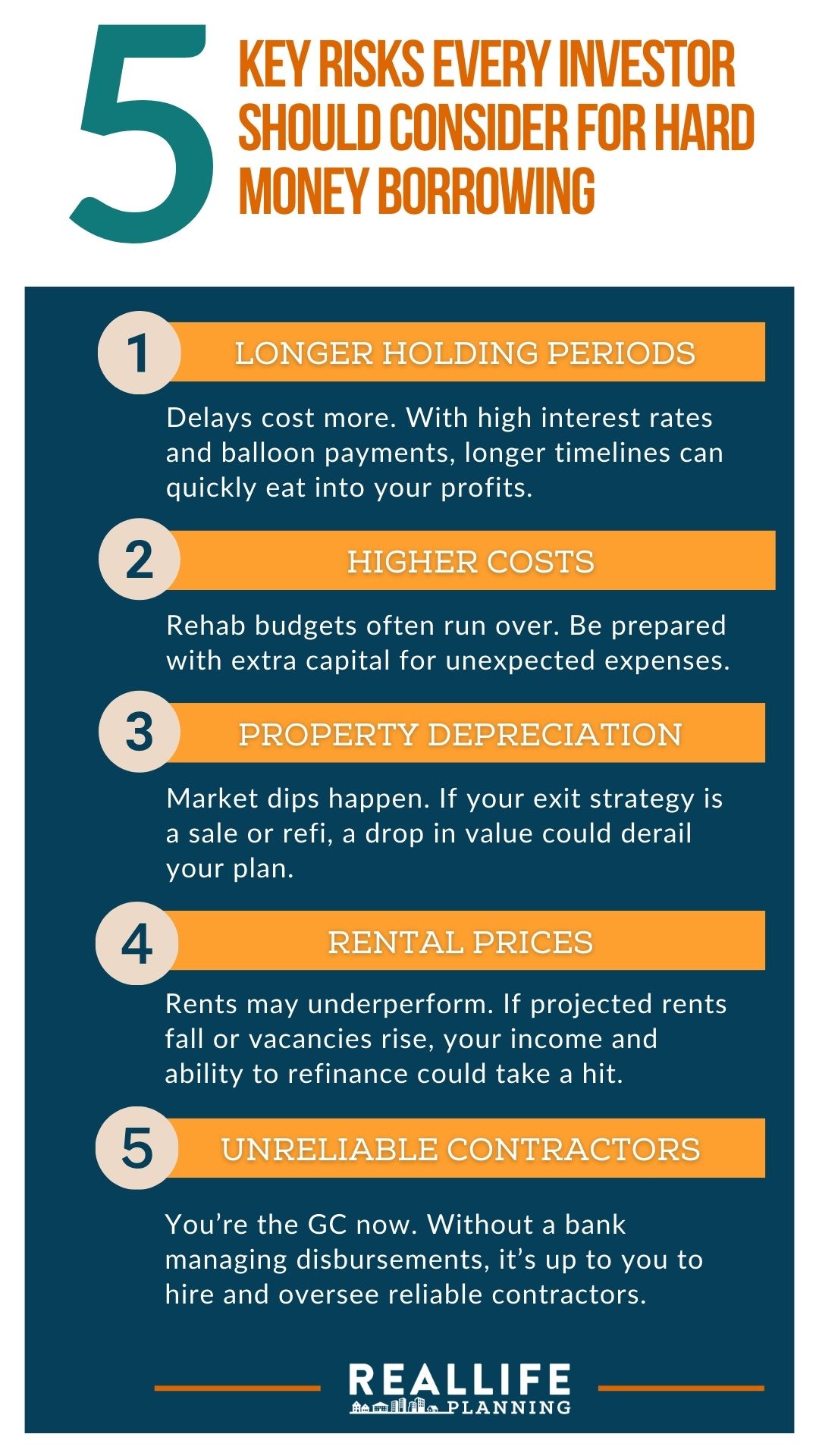

Longer Holding Periods

Longer Holding Periods

The first is the costs of a private loan if the holding period is longer than expected. Interest is typically interest-only during the initial period with a balloon payment at the end, so these costs can add up quickly if a project takes longer than projected. This effect is amplified by the higher hard money loan rates.

Higher Costs

The costs of rehabilitating and renovating the property could also be more than originally expected, which is not an uncommon occurrence in the industry. You’ll want to be prepared for additional costs before working with private lending money.

Property Depreciation

The property you’re investing in could also have depreciating prices. If your exit plan for the project is to sell, or if you plan to refinance to a conventional loan and pay off that hard money loan with a balloon payment at the end of the renovation, you may risk losing money on the project if the value goes down.

Rental Prices

If you're renovating and renting, it’s possible you could have decreased expected rents. There may be certain assumptions of how to service the loan and the eventual refinance mortgage baked into your project plan, but if the market moves against you and the rent turns out to be lower or the vacancy rate is higher, you could be losing some of that projected income on the property.

Unreliable Contractors

You could also have inexperienced or unreliable contractors. As opposed to a traditional construction loan where the bank is your partner in keeping the contractors on track, it’s up to you to pick and manage your contractors in a private lending money situation. They may not be able to deliver in the time allowed for the project budget that you've borrowed for.

The good thing is that a good private lender will help you budget and evaluate your project, so they can be a valuable partner in figuring out whether the post-renovation value of the project might be profitable.

Common Questions That You Should Ask if Considering a Hard Money Loan

There are a few questions that you want to have in mind when considering hard money borrowing.

What are the goals of the project?

You may want to start with the end in mind. What’s your goal for the project? Are you planning to renovate and rent? Or renovate, rent, and refinance?

Are you planning to sell the property? Is this a traditional fix-and-flip? Are you planning to get in, make renovations, get out as soon as possible, and not refinance that hard money loan, just sell it and pay it off?

Knowing your goals for the project can help you direct the decisions that you make with your private lender.

Will the private lender review the property with you?

Experienced hard money lenders have seen many of these kinds of projects, from renovation projects to fix-and-flips to BRRRR projects (Buy, Rehab, Rent, Refinance, Repeat). It may be helpful to have them review the property and the project budget with you so they can give you helpful feedback about whether or not your budget or spending plan for the project is on track (and realistic).

You may also want to ask your lender if they have modeled a range of potential situations. In your risk management, you want to create a kind of worst-case, best-case, and a median-expected-case scenario for your spending and exit plan for the project.

You should have modeled a range of scenarios, and if possible, have discussed this with the hard money lender so that everybody is on the same page about the project.

Do you have other sources of liquidity if the project goes awry?

There may be a situation where you have unexpected construction costs, or it takes longer to sell the property or refinance the loan than expected. It’s important to check with yourself: what other sources of liquidity do you have?

- Do you have cash reserves in your rental property business or your personal emergency fund?

- Do you have access to a HELOC on your home that you could tap into if needed?

- Could you borrow against a taxable brokerage account, or liquidate some securities to pay for an unexpected expense?

- Do you have access to a 401(k) loan (for extreme circumstances) or a cash-value life insurance loan?

You’ll want to make sure you have other sources of liquidity that you could use to pay extra interest costs if the loan period is longer, or extra project costs if the project goes over budget.

H4: What due diligence have you done on the lender?

There are plenty of options when it comes to private money lenders, but you want to know that the lender you’re working with is reliable.

You could start by seeing if they have references from other real estate investors about their work with the lender. You should also be interviewing the lender to be sure that they’re the right match for the project and your goals.

You also want to read all of your documentation and the loan agreement extremely carefully. It’s crucial that you understand what you’re working with before you take out a hard money loan.

H4: Have you had an attorney review your documents?

Under all circumstances, you want to have a legal or attorney review of the loan documents. A loan document is a long and complicated legal agreement, and you must understand it completely.

The costs of having a real estate attorney review this document with you are going to be well worth it, because you'll fully understand what the agreement entails. This will also make it clear what the potential downsides are for you, and what you're on the hook for if things don't work out with your real estate project.

H4: Do you understand the tax implications of the project’s holding period?

These projects can sometimes be spread across multiple years, meaning they may be spread across multiple tax years. It’s critical that you know, and have accounted for, the tax implications of the project before you take on the loan.

Bottom Line

Hard money loans are a short-term financing solution for real estate investors when they may not be able to borrow traditionally. These loans are typically used for “renovate and rent” and “renovate and sell” (fix-and-flip) projects. Hard money loans usually have much higher rates than conventional loans, but allow for quicker closing times and flexibility.

Before taking on a hard money loan, you want to be mindful of your goals for the projects, the legal and tax implications of the private loan, and potential scenarios that may require additional liquidity or capital for the property. You also want to model a range of potential scenarios and perform your due diligence on the lender before moving forward with the transaction.

To learn more about real estate investing, check out The Real Life Blog.

If you want to learn more about how you can work with a real estate financial planner to see if hard money borrowing is the right financing option for you, schedule a call with our team today.