Do Real Estate Investors Need a Living Trust?

Financial PlanningBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

What is a living trust? Do you need one as part of your estate plan if you're a real estate investor?

A revocable living trust is a legal document that allows you to decide how your assets will be managed and distributed after you pass away. This is generally a private process, as assets in a living trust are not included in the probate of an estate.

You, the grantor, create the trust and name both beneficiaries (the people who will inherit your estate or income from it) and trustees, who will manage those assets for the beneficiaries. The trustee and the beneficiary can be different people, giving you flexibility to design exactly how your estate is handled.

Unlike an irrevocable trust, a revocable living trust can be changed, updated, or even revoked during your lifetime. This flexibility makes it an attractive option for many families and real estate investors who want control without permanently giving up ownership.

While a living trust can be a powerful estate planning tool, it’s also complex and time-consuming to set up properly. It’s best drafted by an experienced estate planning attorney, who can tailor it to your family structure, real estate holdings, and long-term goals.

When a Living Trust Makes Sense for Real Estate Investors

There are several financial planning situations where creating a living trust may make sense, especially for real estate investors and families who want more control and privacy in their estate plans.

Blended Families and Custom Inheritance Plans

Blended Families and Custom Inheritance Plans

One of the most common reasons to create a living trust is if you or your spouse has children from a previous marriage.

If you and your spouse have children from previous relationships, setting up a living trust allows you to specify who inherits what, for how long, and under what circumstances. For example, you might assign income to a surviving spouse for a period of time, and then have the assets pass on to children from your previous relationship.

This kind of customization can be especially helpful in a blended family, where you want to make sure everyone is cared for according to your wishes.

Privacy and Avoiding Probate

Another reason to create a living trust is privacy. When someone passes away, their estate usually goes through a public court process called probate, which determines how assets are distributed. Probate is documented, time-consuming, and can be costly for survivors. A living trust bypasses probate entirely; any assets titled in the name of the trust will pass privately and efficiently to your beneficiaries.

Business Continuity for Real Estate Investors

Business Continuity for Real Estate Investors

For real estate investors, this can be especially important. A living trust allows your successor trustee, whether that’s a spouse, adult child, or institution, to immediately step in and manage your rental properties and business accounts.

This means there’s no delay in collecting rent, paying bills, or handling maintenance. Many investors even title their LLC membership in the name of the living trust to make estate settlement easier.

High-Net-Worth Estate Planning

Finally, for those with substantial assets, trusts can also help with estate tax planning. Under the OBBBA, individuals can pass $15 million (or $30 million per married couple) without paying estate taxes, starting in 2026. This will be indexed annually for inflation beginning in 2027.

When a Living Trust May Not Be Necessary

A living trust isn’t always worth the time or expense. If you own most of your net worth in retirement accounts and your primary residence, there may be simpler and less costly ways to handle your estate planning needs.

That’s because retirement accounts such as 401(k)s, IRAs, Roth IRAs, and HSAs pass directly to your heirs through beneficiary designations, not through probate. As long as you’ve named both primary and contingent beneficiaries, those assets will likely transfer smoothly without needing to be placed in a trust.

Many married couples in this situation also hold their primary residence as joint tenants with right of survivorship, which automatically passes ownership to the surviving spouse.

Common Mistakes and Implementation Tips

Common Mistakes and Implementation Tips

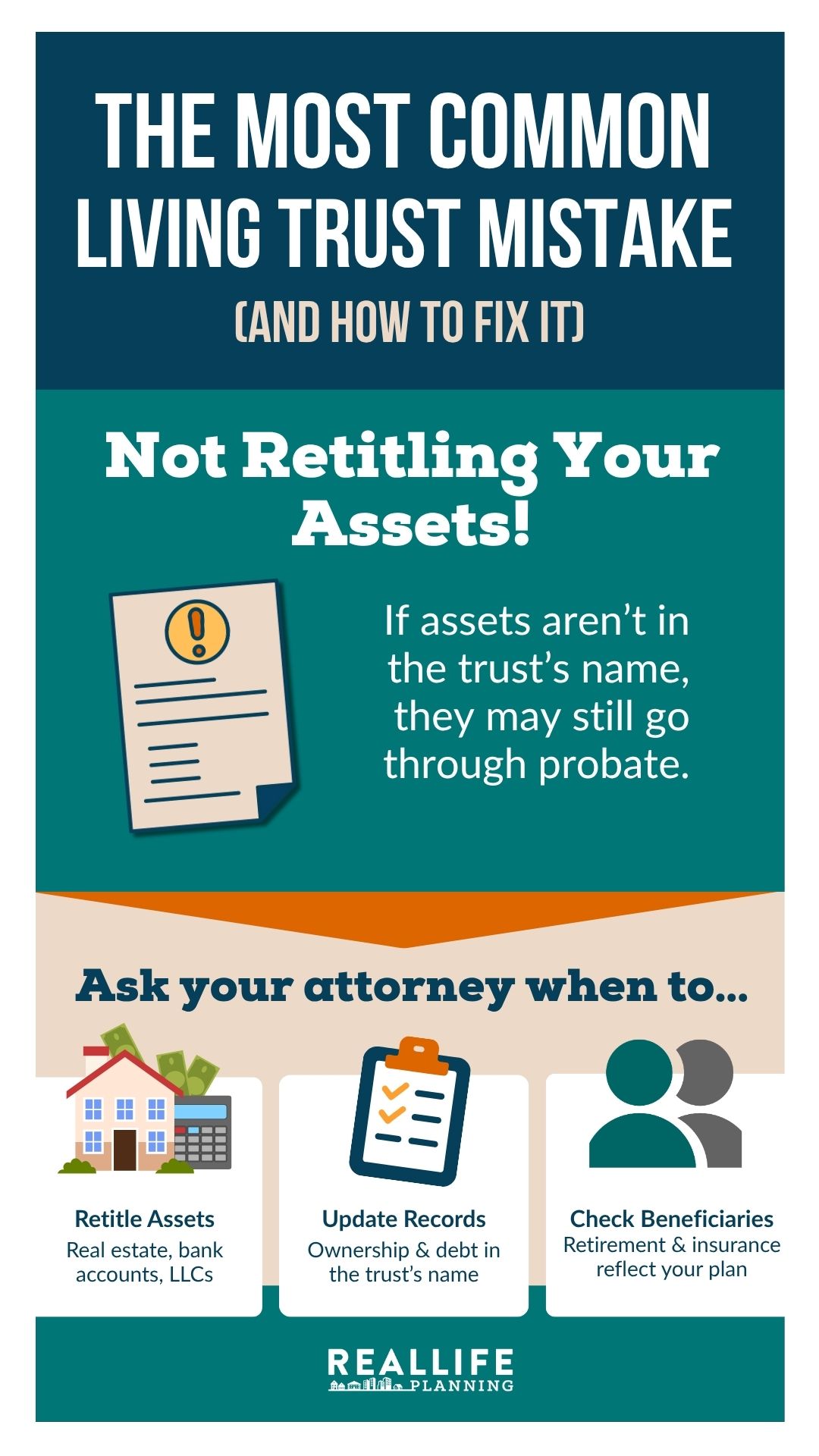

As a real estate financial planner, one of the biggest mistakes I see people make with a living trust is failing to retitle their assets after it’s created.

One important thing to remember: simply creating a trust isn’t enough. A trust only works for assets that are actually retitled in the name of the trust. If you never change ownership on your accounts, real estate, or business interests, those assets will still go through probate, defeating one of the main purposes of setting up the trust in the first place.

Once your living trust is established, make sure to retitle non-retirement accounts, such as bank or brokerage accounts, as well as real estate, vehicles, and business entities like LLCs, in the name of the trust, according to your wishes. Check that all debt and ownership records reflect the same information.

At the same time, confirm that your beneficiary designations on retirement accounts and insurance policies are accurate and up to date. These assets typically transfer by law to named beneficiaries rather than through the trust.

Taking the time to properly implement your trust ensures that your estate plan works the way you intended: avoiding delays, confusion, and unnecessary court involvement for your family.

The Cost-Benefit Consideration

A living trust can be a powerful estate planning tool, but it does take time, money, and professional support to set up properly. Drafting a long legal document, retitling assets, and coordinating with financial institutions all require some investment of effort and cost.

Trusts aren’t just for the wealthy, but they should provide enough value and clarity to justify the expense. For some people, simpler estate planning tools may be more suited.

Before moving forward, it’s best to talk with both a trusted financial planner and an estate planning attorney. They can help you decide whether a living trust makes sense for your situation and ensure you’re getting your money’s worth from the process.

How to Get Started

If you’ve decided that a living trust might make sense, start by talking with your financial planner to discuss your goals and what you’d like your estate plan to accomplish.

If you’ve decided that a living trust might make sense, start by talking with your financial planner to discuss your goals and what you’d like your estate plan to accomplish.

If you’re an employee, check whether your employer offers legal benefits. These programs can often connect you with local estate planning resources. You can also ask other real estate investors for attorney referrals or recommendations.

While online or DIY trust kits exist, I generally recommend working with an experienced estate planning attorney, especially if you own rental properties or multiple business entities. Professional guidance helps ensure your trust is both complete and enforceable.

Bottom Line

A revocable living trust can simplify estate settlement, protect your family’s privacy, and ensure business continuity for real estate investors. It’s especially valuable for blended families, those with multiple properties or LLCs, and households approaching the federal estate tax threshold.

That said, a trust isn’t necessary for everyone, particularly if most of your assets are held in retirement accounts or a primary residence.

The best first step is to consult trusted professionals — your real estate financial planner, accountant, and estate attorney — to decide whether a living trust fits into your overall estate plan and long-term financial goals.

If you have any questions that you'd like to see us talk about regarding financial planning for real estate investors, just leave them in the comments below or email us at: podcast@reallifeplanning.com

This blog is for general financial education purposes. Information contained in this blog should not be construed as financial, tax, real estate, legal, or investment advice. For educational purposes, blog posts may contain links to other websites which are not under the control or and are not maintained by Real Life Planning. Real Life Planning has provided those links for your convenience but does not necessarily endorse all the material on those sites. Please consult your financial, real estate, legal, or tax advisor for advice specific to your situation.