Does the 1% Rule Work in Today's Real Estate Market?

Real Estate CoachingBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

If you’re a real estate investor, you’ve probably heard of the 1 percent rule, which suggests that if an investor calculates what 1% of the cost of a property’s purchase price (plus necessary renovations to get it rented), they’ll have a monthly rent figure that covers or exceeds a property’s mortgage and expenses. If market rents for similar properties are at that 1% level or above, it’s generally worth running an analysis on individual properties.

While the 1% rule is one of the most widely referenced guidelines for new real estate investments, offering a quick way to decide whether a deal is worth a full analysis, it raises the question: Does the 1% rule still work?

In this article, we’re going to break down what the 1% rule is, where it can still add value, and how to more broadly evaluate rental property investments.

What is the 1 Percent Rule in Real Estate Investing?

The 1% rule is a “rule of thumb” that says a rental property will generally be profitable if your monthly rent is 1% or greater of the purchase price plus the renovation costs that are necessary to make the unit rentable.

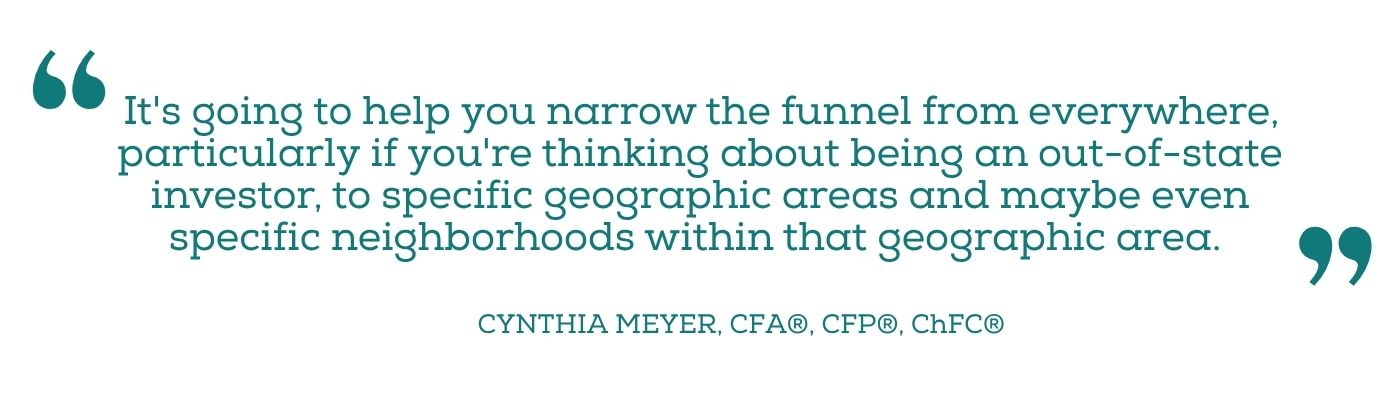

It’s a screening tool that can help investors decide if a closer look is worth their time. By the time investors get to their local market expert, they’re usually way past the point of using this rule; the 1% rule serves more to help them decide if they even want to be in a market.

This is especially helpful early in the process, when you’re comparing different markets or trying to decide where to focus. It can help answer questions like:

- Is this market worth exploring further?

- Does this deal justify running a full analysis?

This rule can help investors in earlier stages to narrow down the funnel and decide where it makes sense to start looking for properties. It’s for investors asking the question, “Do I want to invest in Milwaukee, Salt Lake City, or Detroit?”

Applying this rule helps them figure out a good place to start within a geographic area, but it doesn’t determine whether a property is a good or bad investment on its own.

Does the 1% Rule Still Work Today?

A question that we hear a lot in the space is whether the 1% rule is still valid in this market.

A question that we hear a lot in the space is whether the 1% rule is still valid in this market.

In today’s market, many investors are finding that hitting the 1% threshold (especially on new purchases) is becoming much more difficult than it once was. In many cases, these deals may be bringing in closer to 0.8% (or 80 basis points) than the full 1%.

In this market, house prices are increasing faster than rents are, particularly in the single-family market. The gap between purchase price and achievable rent has widened, making it harder for property owners to meet that traditional 1% benchmark.

That doesn’t necessarily mean that the rule no longer applies at all, but it does mean that it needs to be applied with more context.

In some cases, a property may not meet the 1% rule at the time of purchase, but can move closer to it over time.

For example, take our 2021 1031 exchange from a single-family home into a duplex in the Detroit metro area. We bought the replacement property for about $330,000, and this was not initially a 1% property, but closer to a 0.8% property with the existing leases.

Over about 18 months, we were able to raise rents to market with vacancies and new leases. That rental income changed to almost $3,600 a month in gross rent on that initial $330,000 investment. Sometimes it takes a little time and patience to get to that threshold.

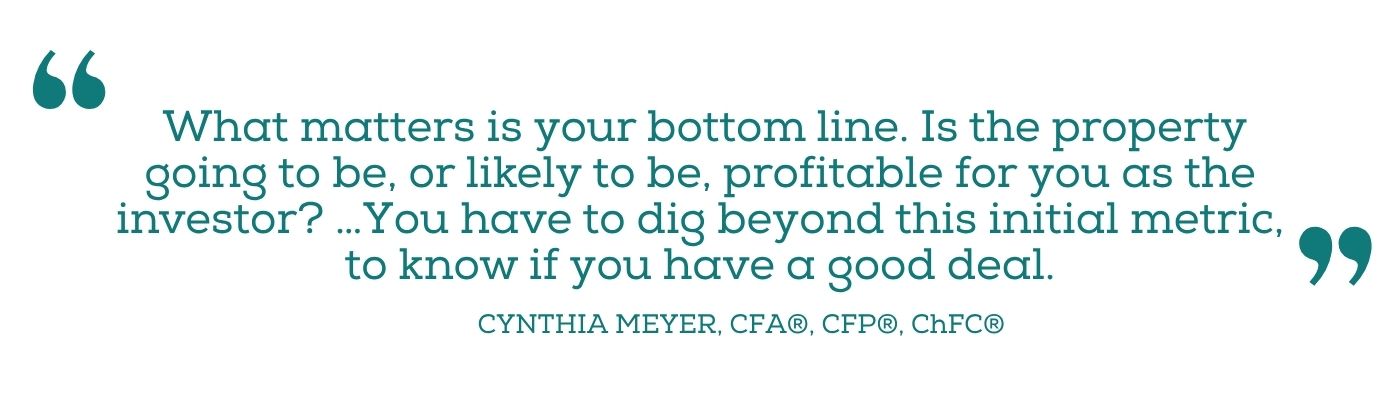

Outside of any one rule, the most important thing to focus on is whether a property is likely to be profitable for you as the investor. Focusing on the net, not gross, cash flow can help you decide if you have a good deal for you.

Financing costs, maintenance and utilities, and property management expenses will all play a role in the profitability of an investment property.

Factors that Can Impact a Property’s Profitability

Once you move beyond a high-level guideline like the 1% rule, you can determine profitability by looking at the combination of variables that can significantly vary from one property to another.

Once you move beyond a high-level guideline like the 1% rule, you can determine profitability by looking at the combination of variables that can significantly vary from one property to another.

Understanding these factors is what helps you as an investor to get a more realistic view of how a property may perform over time.

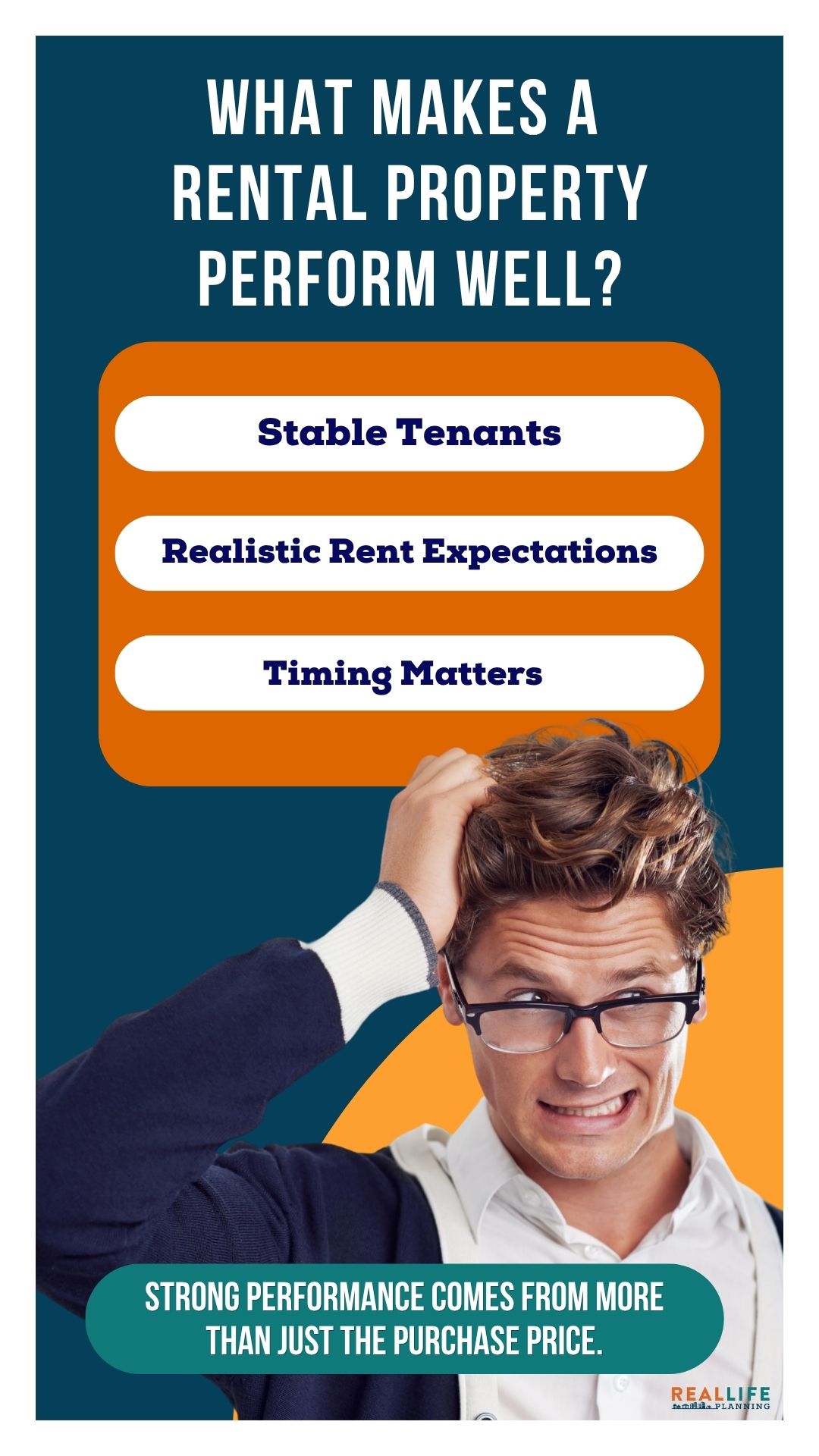

Vacancy and Tenant Quality

One of the major factors that affects the profitability of a property is how consistently it will remain occupied.

It’s not just about whether you can find a tenant, but about how long it takes, how often there is turnover (and what the timeline looks like), and the quality of the tenant you’re able to place. Many investors look for tenants earning at least 3 times the monthly rent to reduce the risk of missed payments or early turnover.

If a property is vacant longer than expected, or if tenants cycle in and out more frequently, that can have a negative impact on your cash flow.

Realistic Rents vs. Projections

Another factor that can really have an impact on profitability is relying too heavily on projected or “ideal” market rents.

While data and comparable properties can provide a useful benchmark, the reality on the ground can look very different. A property might be modeled at $1,500 per month, but if similar units in the area are struggling to rent at $1,400, that can make a significant difference in what you may be able to collect.

Every market has natural ceilings, and pushing beyond what tenants are willing or able to pay can lead to longer vacancy periods or the need to reduce rent after the fact.

Timing of Rent Increases

Rent levels don’t stay static, and timing plays an important role in how well a property performs, especially early on.

If a property is tenant-occupied at below-market rates, there may be an opportunity to increase rent over time. That increase, however, often depends on tenant turnover, which means this may not be immediate.

This tends to be responsible for a gap between initial performance and long-term potential. A deal may seem less attractive at acquisition, but improve as rents adjust to market levels. It’s helpful to factor in that timing to create a more realistic view of both short-term and long-term performance.

Cash Flow vs. Appreciation

One thing that’s important to get clear about is what you’re optimizing for.

One thing that’s important to get clear about is what you’re optimizing for.

Not all real estate investments are designed to perform the same way. In many cases, there’s a tradeoff between cash flow and appreciation of the property. Understanding where an investment falls on that spectrum can help to shape your expectations beyond the 1% rule.

Some markets offer stronger cash flows from the start, with rental income that more comfortably can exceed expenses. Others may offer lower initial cash flow, but greater potential for long-term appreciation.

Neither approach is necessarily better; it just depends on your goals.

For some investors, immediate cash flow is more of a priority than long-term wealth building. These investors tend to look for properties that generate consistent cash flow and can support current financial needs. These opportunities are often found in markets where purchase prices are lower relative to rents, but where long-term appreciation might be more modest.

For those more focused on building wealth over time, an investor may be willing to accept lower (or even neutral) cash flow in exchange for stronger appreciation potential over the long term.

Think of cash flow as the cake, and appreciation as the frosting. Both can play a role in an investment strategy, but the balance should reflect your overall financial goals and time horizon.

Consider Local Expertise

As investors start looking at more detailed analysis than the 1% rule, understanding neighborhood trends is really important in deciding the profitability of a property.

This is where local expertise becomes even more valuable.

Within any given market, there can be huge differences from one neighborhood to another. Factors like tenant demand, rental pricing trends, turnover rates, and long-term development can all differ — sometimes even from a few miles away.

A local perspective can help investors better understand those dynamics and identify opportunities that may be a fit for their specific goals, whether that’s stronger cash flow, long-term appreciation, or a balance of both.

Build Your Investment Criteria

One of the biggest takeaways from this discussion is that there is no single “right” metric that will apply to every investor.

While guidelines like the 1% rule may be helpful, they’re only one piece of a much larger decision-making process. What ultimately matters is how a particular investment property fits within your own financial goals, risk tolerance, and time horizon.

Some investors may prioritize the 1% threshold as a baseline for cash flow, while others may be comfortable with a lower starting point if the property offers stronger appreciation potential or fits into their long-term strategy.

Having a clear set of criteria that reflects what you’re trying to achieve can help you evaluate potential properties. This might include target returns, acceptable levels of risk, expectations around cash flow, your desired holding period, financing considerations, etc.

Run Your Own Numbers

The 1% rule can be a helpful part of the investment process, but only when it’s used in the right context.

Rather than using it as a single decision-making tool, it works best to serve as an initial filter to help you decide if a full budget analysis on a particular geographic area and particular deal may be worth it.

It’s important to run your own numbers to make sure a property may work for you and that all potential variables are accounted for. This means looking beyond gross rent and focusing on net cash flow, factoring in financing costs and maintenance, considering vacancy rates, and other real-world factors that may ultimately determine how a property will perform.

If you’re a real estate investor looking to learn more about real estate investing, check out some more insights from Real Life Planning.

This episode in the Rental Property Cafe is a great place to start if you’re interested in building and growing your real estate portfolio.

If you have any questions that you'd like to see us talk about regarding financial planning for real estate investors email us at: podcast@reallifeplanning.com

This blog is for general financial education purposes. Information contained in this blog should not be construed as financial, tax, real estate, legal, or investment advice. For educational purposes, blog posts may contain links to other websites which are not under the control or and are not maintained by Real Life Planning. Real Life Planning has provided those links for your convenience but does not necessarily endorse all the material on those sites. Please consult your financial, real estate, legal, or tax advisor for advice specific to your situation.