Financial Planning Steps Before a 1031 Exchange

Real Estate CoachingBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

| 🏠 | the importance of 1031 exchanges in scaling a real estate portfolio |

| 🏠 | 1031 exchange deadlines |

| 🏠 | role of the Qualified intermediary |

| 🏠 | what is a reverse exchange? |

A 1031 exchange can be a powerful way for real estate investors to defer taxes; however, without careful financial planning, it’s possible to make costly mistakes that can derail your long-term goals.

That’s why we’re sharing our top financial planning steps as an educational resource for those considering a 1031 exchange for real estate assets.

What is a 1031 Exchange in Real Estate?

A 1031 exchange comes from IRS Section 1031, and it allows taxpayers to defer the taxation (or the recognition of a capital gain) if proceeds are invested in a like-kind property.

When a 1031 exchange occurs, the adjusted basis carries over into the new property. This means that the original purchase price of the property that you sell — adjusted for improvements and depreciation — carries over into the replacement property.

Why is this so important in real estate investing?

1031 exchanges allow investors to reinvest the entire proceeds from the net cost of sale into a new property, which can be especially valuable for an appreciated property. This allows investors to scale their real estate portfolio faster and more efficiently.

This also allows real estate investors to borrow beyond what their original borrowing amount was for the property sold (or the relinquished property) to buy a replacement property that may be larger or have more doors to generate more cash flow.

If used correctly, 1031 exchanges can be a powerful strategic tool in real estate investment businesses. This type of tax deferral is a benefit unique to real estate - there is no direct equivalent to a 1031 exchange in securities investing.

What is Like-Kind Property?

According to the IRS, properties are of like-kind if they’re of the same nature or character, even if they differ in grade or quality. For example, you can exchange raw land for a multifamily property or a single-family rental for a commercial building.

Basically, a 1031 exchange allows you to exchange one kind of real estate property for another, as long as the property meets this standard, which provides a relatively broad ability to exchange a property for a replacement.

What is NOT a 1031 Exchange?

Since IRS Section 1031 defines a like-kind property as one of the same nature or character, you can’t, for example, exchange a rental property for a financial planning business.

Since IRS Section 1031 defines a like-kind property as one of the same nature or character, you can’t, for example, exchange a rental property for a financial planning business.

1031 exchanges also cannot be for personal use, only for a property used in a trade or business investment for business purposes. This means that you cannot 1031 exchange your single-family home that you live in. This also applies to properties that you plan to use entirely for a personal vacation property.

Another key consideration with 1031 exchanges is that the exchange must be from a taxpayer (or taxpayers) to the same taxpayer(s). If you individually own a property, you must exchange the property for another that will be held individually.

In the same manner, if you own a property as joint tenants with your spouse, the replacement property must also be held as joint tenants wth your spouse.

Ownership Structures for 1031 Exchange Real Estate Property

Investors may want to consider the corporate structure of their real estate investment business, preferably years in advance of making a 1031 exchange.

For example, if, in the long run, you want your properties in a limited liability company (LLC), you want to make sure you set that up a year or more before you intend to 1031 exchange a property. Make sure to get legal advice from your attorney on this.

Sometimes, problems can arise when co-owners don’t share the same goals, like if one party of a divorcing couple who owns a property as joint tenants with right of survivorship decides they want to do a 1031 exchange, and the other doesn’t.

What some investors decide to do in this situation is to switch from a joint tenants with right of survivorship to tenants in common structure to extricate themselves from a business partner. If this is something that you want to consider, you want to make sure you’re setting this up a year or more in advance of a 1031 exchange.

These decisions have legal and tax implications, so please consult your attorney and accountant well ahead of any planned 1031 exchange to ensure the structure supports your long-term goals.

What Qualifies for a 1031 Exchange

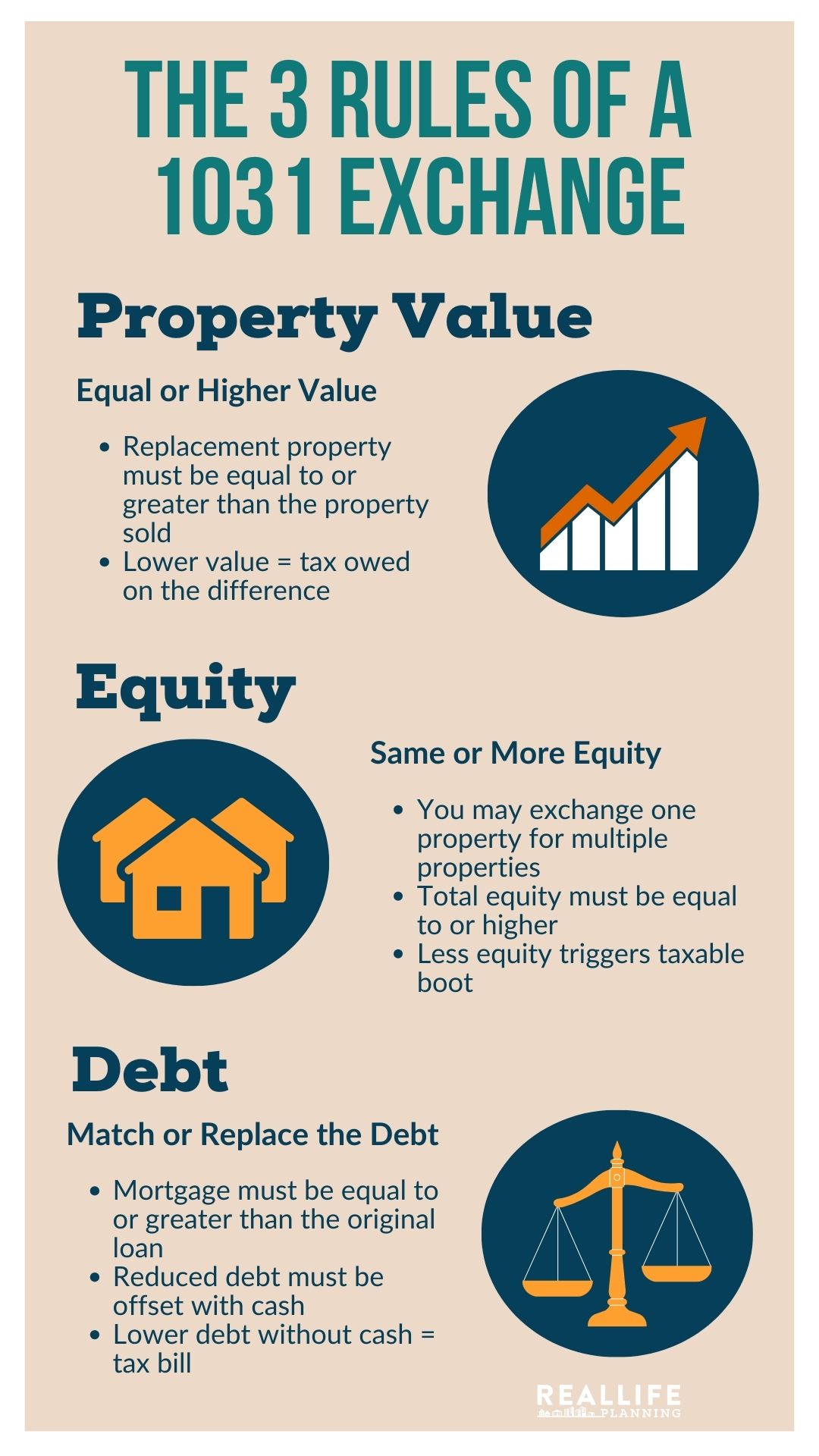

To be fully tax-deferred, the replacement property for a 1031 exchange must be of equal or higher value to the relinquished property. If the value is not equal to or higher than the relinquished property, you will need to pay taxes on the difference.

You can exchange one higher-priced property for multiple lower-priced properties in this situation, as long as you have the same amount of equity or higher and the same amount of debt or higher under the 1031 exchange.

You can exchange one higher-priced property for multiple lower-priced properties in this situation, as long as you have the same amount of equity or higher and the same amount of debt or higher under the 1031 exchange.

The replacement property must also have a similar leverage structure, unless you can put some cash into the investment in place of loans. The mortgage on the replacement property must match the loan amount on the relinquished property (or can exceed it, if you are buying a more expensive property), unless you add cash to cover the difference. If either the equity or debt is lower than the relinquished property, you’ll owe tax on the difference.

What if the Relinquished Property is Worth More?

If you’re making an unequal exchange where the relinquished property is worth more than the replacement property, or you take less of a loan with the replacement property, you're going to pay taxes on what is called “boot”.

Boot is defined as the money or the fair market value of other property that's received by the taxpayer in a 1031 exchange. It includes all of the cash equivalents, plus liabilities that are assumed by the other party or liabilities to which the exchanged property is subject.

A common misconception is that some investors think they can just 1031 exchange the equity part, but not the loan part, of the property they’re selling. This, unfortunately, is not true. In reality, both equity and debt must be equal to or greater than in the relinquished property, or you’ll pay taxes on the difference.

Time Limits on 1031 Exchanges

1031 exchange rules come with very strict time limits. As a real estate financial planner, I encourage clients to start planning well in advance of putting the relinquished property on the market.

When you sell the original property, you have 45 days from the sale of the relinquished property to close on a replacement property or identify properties. The money from the sale of the relinquished property is held by a Qualified Intermediary during the 1031 exchange process until the end of those 45 days.

You also have only 180 days from the day of the original sale to close on any properties that you have identified by day 45.

Practically speaking, here’s what that looks like: you sell your relinquished property, the money goes to the qualified intermediary, and you're sitting there with cash.

You can buy as many replacement properties as you like between day 0 and day 45 and close on them before the end of day 45. If you have any of the funds left over from the exchange, or have not closed a sale on day 45, then you must identify up to three replacement properties under the most commonly used identification formula, and you have to close on one of those replacement properties by the 180th day.

What Are the Rules of a 1031 Exchange?

The deadlines of a 1031 exchange are very strict and non-negotiable. There are a number of ways to meet that window, but the most common identification formula is called the “3-property rule”. This rule says you can identify three properties of any value within the first 45 days, but you have to close on one of them within 180 days after the sale of the original property.

This is why you must be sure to know what you want to buy as a replacement property before you even sell your relinquished property, because the short, strict timeline can be difficult to accommodate in real estate unless you’re doing an all-cash transaction.

If there is a complex exchange or somebody is exchanging a whole portfolio of properties for another portfolio of properties, there are other identification rules, such as the 200% rule or the 95% rule; however, unless you’re a sophisticated investor with a large portfolio, these likely will not apply.

What is a Qualified Intermediary?

Another key consideration that you want to plan for before initiating a 1031 exchange is identifying a qualified intermediary. This intermediary cannot, under any circumstances, be you, as any person who is the exchanger is a disqualified person.

Typically, qualified intermediaries are law firms or professional 1031 exchange companies that specialize in these transactions and understand real estate transactions and taxation. A qualified intermediary acts like an escrow agent. They hold the funds for you and prevent you from accessing the funds transferred during the exchange, so as not to violate the like-kind property rule.

Typically, qualified intermediaries are law firms or professional 1031 exchange companies that specialize in these transactions and understand real estate transactions and taxation. A qualified intermediary acts like an escrow agent. They hold the funds for you and prevent you from accessing the funds transferred during the exchange, so as not to violate the like-kind property rule.

In simple terms, a qualified intermediary is somebody who holds the money in escrow for you, and when you're ready to buy the replacement property, they will directly send that money to closing on the replacement property. This does add some paperwork and bureaucracy to the process, so it’s important to be respectful of deadlines and communicate in advance with your 1031 intermediary.

At the end of the day, everyone (including real estate agents) on both ends of the transaction needs to understand that this is a 1031 exchange and what the deadlines are.

What is a Reverse 1031 Exchange?

Another avenue with these transactions is a reverse 1031 exchange, when you buy the replacement property before you sell the relinquished property.

These are typically more expensive transactions than typical forward exchanges, so it only makes sense when there is a very large capital gain that you’re looking to defer, and when you have clearly identified the replacement property before you’ve even put the relinquished property on the market.

These transactions are not as common and not always as applicable to real estate investors’ situations, but it’s helpful to think about and speak to your real estate financial planner and accountant about it, if it’s something you’re interested in.

In either case, you will still want to know well in advance of doing a 1031 exchange (traditional or reverse) what your plans are for the exchange.

Final Thoughts

1031 exchanges can be a valuable tax-deferring tool for real estate investors looking to sell one property in exchange for another. Before you complete a 1031 exchange, however, you want to be prepared long before you’re ready to put your property on the market.

First, it’s important to know what your end goal is:

- Are you trying to exchange into a more expensive property with a higher cash flow and more doors?

- Are you exchanging for a property in another state?

- Do you have goals of ending up in a different corporate structure?

Whatever the case is, you have to execute on your goals well before you sell the relinquished property, and you cannot wait and do these things at the same time as the 1031 exchange.

You also must be sure that the property you’re looking to exchange into is of like-kind, so it must be similar in nature or character. While this is a pretty broad definition in the real estate space, certain types of real estate investments such as syndications are typically not available as like kind replacement properties.

By using the appreciated value to have a higher down payment on a more expensive property (possibly with more doors and a higher cash flow), investors can scale or build their portfolio with this tool.

It’s also important to know that the original basis of the property that you sold carries over on an adjusted basis to the new property, so this is not the time to “DIY” your taxes. As always, you want to consult with your CPA or tax advisor on any potential tax strategies. It's important to get well ahead of those decisions before being in a time-sensitive situation, so that you can optimize your tax situation for the long term.

If you have a property that is highly appreciated or that you're thinking about selling, you certainly want to discuss this, not just with your REALTOR®, but with your real estate financial planner and your accountant.

You may want to do this up to a year in advance of exchanging, so that you can work through some of these questions and decide if any changes need to be made, what your strategic goals are for the 1031 exchange, and that you fully understand the taxation of whatever is not going to be exchanged. This way, you're not caught unaware with the tax bill after the exchange, and can think through your strategic goals for the process.

If you want to learn more about financial planning for real estate investors and see how our team at Real Life Planning can help you, we’d love for you to schedule a call with our team. To learn more insights about real estate investing from a CERTIFIED FINANCIAL PLANNER™, you can see more from the Real Life Blog or our podcast episodes.