Life Insurance Policy Loans: Pros and Cons for Real Estate Investors

Financial PlanningBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

How can real estate investors use life insurance to provide liquidity for their next real estate purchase or renovation, or to create retirement cash flow later on?

You likely hear radio commercials all the time, promising tax-free retirement income without any stock market risk. Maybe you’ll sign up on a site where an agent will get you on a call to talk about using your whole life insurance or universal life insurance for tax-free retirement income, where things sound just a bit too good to be true.

Can permanent life insurance really be a retirement plan, or a way to create your own “bank”? In this article, we’re going to talk about life insurance policy loans, what they’re designed for, what they’re not designed for, and how they may potentially fit into your existing financial plan.

What is Permanent Life Insurance?

Permanent life insurance is primarily designed to protect your family and loved ones who rely on your income to maintain their standard of living. It is not designed for retirement savings or to create your own financial institution.

Permanent life insurance is primarily designed to protect your family and loved ones who rely on your income to maintain their standard of living. It is not designed for retirement savings or to create your own financial institution.

As the name suggests, the protection from permanent life insurance stays with you for your entire life, as long as you pay the premiums. Whether your policy is whole life or universal life insurance, it includes both a death benefit component and a savings component.

While term life insurance has the death benefit component, permanent life insurance adds the savings component through the policy's cash value. With these policies, you pay extra on each premium to accumulate those savings, which can grow tax-deferred.

If you surrender the policy, that cash value component would be paid out to the insurer (as opposed to the beneficiaries in the event of passing).

Is Life Insurance a Retirement Plan?

When we hear people talk about using their permanent life insurance as a retirement plan or financing plan for their real estate cash flows, this means that they’re borrowing against the accumulated cash value of their policy.

While it’s correct that you may borrow against the cash value of your life insurance policy in some circumstances without taxes, and that invested premiums do grow tax-deferred, there are some significant disadvantages to this strategy that you should be aware of before you have a discussion with the insurance agent.

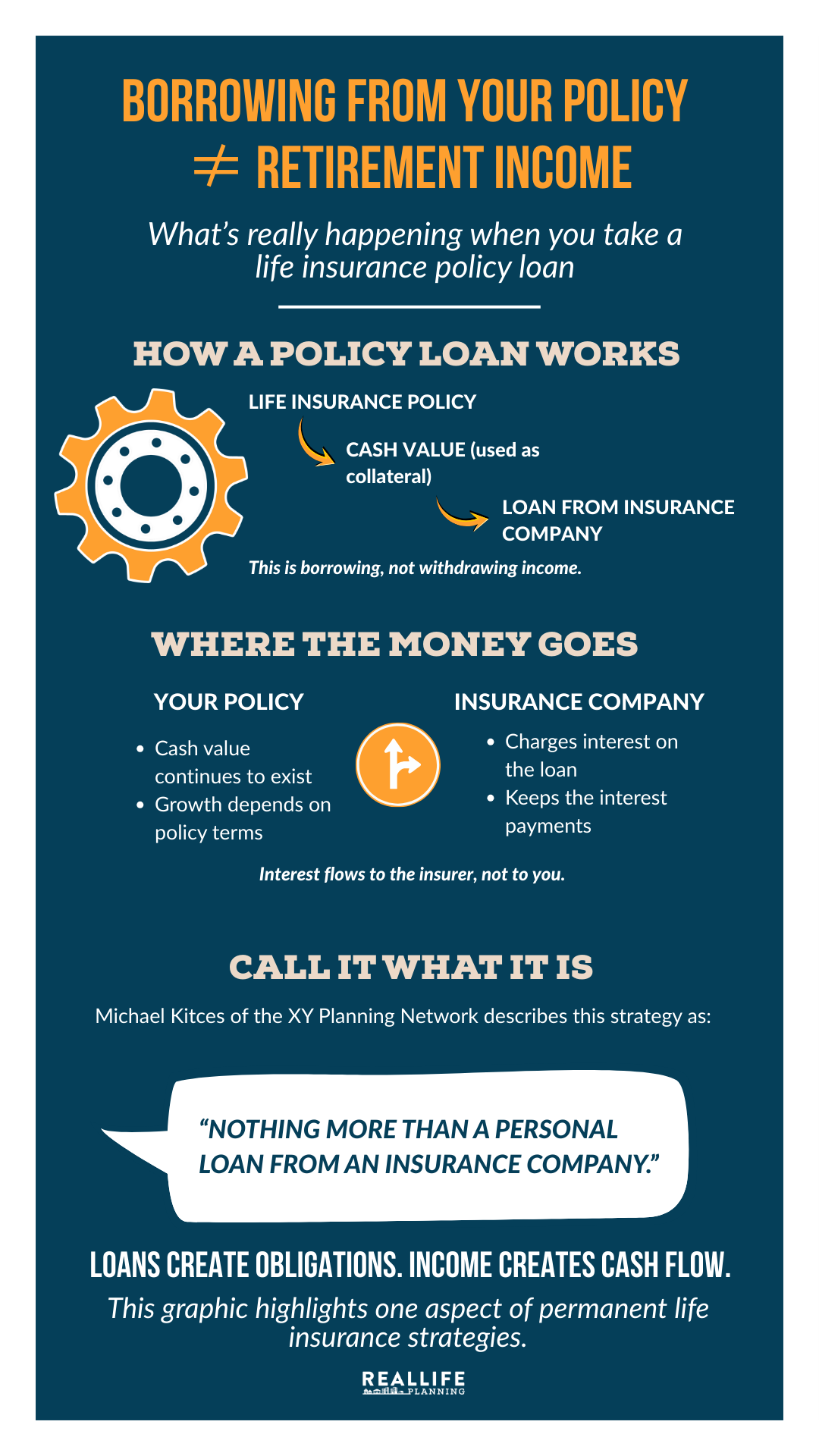

A Life Insurance Policy Loan is Not Income

A Life Insurance Policy Loan is Not Income

The first is that a policy loan is not income. A policy loan uses the cash value of the policy as collateral, and the insurance company charges the borrower interest on the loan. The interest goes to the insurance company here, not you. That interest rate could be the same, higher, or lower than the rate of interest you receive as a policyholder on the growth of the cash value, depending on the particular policy you have.

While this borrowing strategy goes by different names - many of which can be misleading - financial planning expert Michael Kitces calls this borrowing strategy “nothing more than a personal loan from an insurance company.” This is not income.

Dividends are Not Guaranteed

The second potential disadvantage that you should be aware of is that policy dividends from certain types of policies, while helpful, are not guaranteed. Consequently, relying on policy dividends to help with the growth of that cash value may not be a safe or accurate assumption.

Certain types of insurance companies do pay dividends to policyholders who hold what's called a “participating policy”. When they have positive annual results, those dividends can be applied to future premium payments or used to purchase additional coverage. The insurance company, however, will not necessarily make a profit every year to distribute dividends, so these may not be reliable.

Tax Considerations

The other important thing that you should be aware of is potential tax complications that come with a strategy where you’re building up a large cash value and then borrowing large amounts against that cash value. While dividends from participating policies are not taxable, strategies that recommend borrowing against a life insurance policy’s cash value have potential tax problems.

One main strategy that investors sometimes use is to borrow against that cash value temporarily to be in a good cash position to make an offer on a property. They will then complete the deal and refinance it with a regular mortgage to pay back the policy loan.

The other way is using the idea of life insurance for retirement income, where they accumulate a large cash value over time and then just keep taking out policy loans that they never pay back.

Should you borrow enough of your cash value and not pay it back, and the bill for the premiums keeps coming each year, you could have to put the cash back or risk the lapse of the policy if the cash value goes back to zero.

If the policy lapses, the total amount of outstanding loans against that cash value would be included in your taxable income for the year in which the policy lapses.

Life Insurance Fees

It’s also important for investors to remember there is no “free lunch”. One of the biggest disadvantages of using life insurance as a cash flow strategy is that there are many associated fees.

First of all, you have to pay for the life insurance. If you die early, your beneficiaries would receive the full death benefit, which comes with underwriting costs and mortality charges to maintain the life insurance policy throughout your whole life, even though you may end up not needing the insurance protection for your whole life.

You also have to pay for the distribution of the policy, which is a nice way of saying that the insurance salesperson is making a commission for selling you the policy. The fees eat into the returns that you might otherwise receive with that money if you were to invest the money independently, like if you open a low-cost brokerage account and invest that money into tax-efficient funds, for example.

Alternatives to Using Life Insurance with Policy Loans

There are many other alternatives to using whole or life insurance in conjunction with policy loans to create future cash flow for yourself.

Taxable Brokerage Accounts

One option that may fit for people who don’t have a permanent life insurance need is to, over time, fund a taxable brokerage account with well-diversified, low-fee, tax-efficient investing. There are generally index funds, exchange-traded funds (ETFs), and maybe even mutual funds, used to build a low-cost, low-turnover, tax-efficient portfolio over time.

One option that may fit for people who don’t have a permanent life insurance need is to, over time, fund a taxable brokerage account with well-diversified, low-fee, tax-efficient investing. There are generally index funds, exchange-traded funds (ETFs), and maybe even mutual funds, used to build a low-cost, low-turnover, tax-efficient portfolio over time.

This can be coupled with a term life policy or ladder of term life policies that meet your family’s unique life insurance needs. Maybe you only need insurance until your children are well-established in their twenties with their college paid for, or until you have enough retirement savings that you don’t need to leave an estate, should you predecease your spouse.

These are all questions for you to partner with a financial planner who understands real estate and a tax advisor, to create the right combination of these two things to accomplish the same general strategy with much less hassle and more flexibility.

Securities-Based Lending

Many brokerage firms offer securities-based lending against taxable brokerage accounts pledged as collateral. These are often interest-only loans for a set period of time, which then convert to regular amortized loans if not paid back.

Many brokerage firms offer securities-based lending against taxable brokerage accounts pledged as collateral. These are often interest-only loans for a set period of time, which then convert to regular amortized loans if not paid back.

Similar to borrowing on margin, this strategy consists of pledging your securities as collateral for a line of credit or term loan. With a well-diversified, large portfolio, that can be an excellent way to create liquidity without having to sell securities in a tax-efficient manner.

Coupling this strategy with term life insurance, which lasts for the period of time you need coverage, can be a great way to keep your family protected as well.

Final Thoughts

The right strategy for you and your family is going to come down to your unique needs. You may or may not need permanent life insurance; you may be able to build a bit faster with a taxable brokerage account, or you may be open to the risks that come with borrowing against your securities.

Talking through each of these points with your financial planner can help you figure out what strategy interests you and would be the best fit for your particular financial situation. I urge you to consider life insurance in the context of your estate plan.

Again, there are other ways to create future sources of liquidity for yourself without tying yourself up in a long-term life insurance contract that may be expensive and/or not what you need.

How Do You Know if Permanent Life Insurance is for You?

You may need a permanent life insurance policy if you’re a high-net-worth investor and you expect that your estate is going to exceed the limit for passing to the next generation without estate taxes, or maybe if you have a special needs child or stay-at-home spouse, or a closely held business, for example.

These are all important aspects to consider, and there are many cases where you may need permanent life insurance, but you’ll want to make sure you’re making this decision based on your need for the insurance, not whether or not you need a policy loan in the future.

Bottom Line

As with all financial and investment decisions, make sure you know the risks, alternatives, and potential rewards before deciding to sign a contract. I recommend that you take your time, do your research, talk it over with your financial planner, and ultimately make the choice that’s best for you.

If you’re interested in taking out a life insurance policy loan for a real estate investment, we invite you to book a call with our team to learn more about how we work with real estate investors like you.

This blog is for general financial education purposes. Information contained in this blog should not be construed as financial, tax, real estate, legal, or investment advice. For educational purposes, blog posts may contain links to other websites which are not under the control or and are not maintained by Real Life Planning. Real Life Planning has provided those links for your convenience but does not necessarily endorse all the material on those sites. Please consult your financial, real estate, legal, or tax advisor for advice specific to your situation.