Is a Buy and Hold Real Estate Strategy a Good Fit For You?

Real Estate CoachingBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

Is a “buy and hold” strategy the right fit for you?

Real estate investing can be a great long-term wealth-building tool, and “buy and hold” is one of the popular approaches. While it sounds straightforward, there are several ways to implement this strategy — each with different levels of involvement, risk, and capital requirements.

Every investor has a unique situation, with their own tolerance, goals, and ideal holding periods. Understanding the differences between strategies is key to deciding what approach fits your overall financial life.

What is a “Buy and Hold” Strategy?

When investors consider buying and holding, they typically think of “one right way” to do it; however, there are many different ways that investors can implement this strategy beyond one traditional model.

When investors consider buying and holding, they typically think of “one right way” to do it; however, there are many different ways that investors can implement this strategy beyond one traditional model.

Buy and Rent

The most common approach is buying a property and generating income through rent — whether that’s a single-family home, multifamily property, vacant land, or even self-storage.

This strategy is usually appealing for investors looking for ongoing cash flow and longer-term appreciation, but it also comes with responsibilities like property management, maintenance, and tenant-related challenges.

House Hacking

Another variation of the buy and hold strategy is what we call “house hacking”. House hacking is a strategy where investors buy a property and live in part of the property, and rent out other units. Many investors also “house hack” by operating a business in one unit and renting out the others.

Essentially, this strategy allows investors to use one unit – whether for living or another purpose – and generate rent out of the remaining units.

Holding Mortgages

Another way to approach buy and hold real estate is by acting as the lender rather than the property owner.

In this strategy, you’re essentially serving as the bank, providing financing to another investor or homeowner and earning a return through interest payments. This can be done by partnering on a deal strictly as a lender or, in some cases, can have an equity component.

While this approach can provide more predictable income compared to owning property directly, it still requires careful due diligence around the borrower, the property, and the terms of the loan.

Buying Notes

Investors can also participate in real estate lending by purchasing existing loans (or “notes”) on the secondary market.

For example, if another investor has issued a private loan for a real estate project, that loan can be sold to a new investor at a discount. The new note holder then collects the remaining payments from the borrower based on the agreed-upon terms.

Real Estate Securities

Another option is investing in real estate securities, such as real estate investment trusts (REITs) or homebuilder stocks, as well as mutual funds and ETFs that hold them. REITs are companies that own, operate, or finance income-producing real estate and can be traded publicly or privately.

3 Questions to Help You Pick the Right Strategy

Once you understand the different ways to approach buy and hold investing, the next step is figuring out which path actually fits your situation. Here are 3 questions that can help you evaluate what the right strategy would be for you.

Do you want to be hands-on or hands-off?

Part of deciding the right strategy for you is understanding the level of active participation you want to have in the investment. While “hands-on or hands-off” sounds black-or-white, there are many different levels of involvement.

Your amount of time, skill, and interests all play an important role in deciding how hands-on you may want to be in the investment. You may need to evaluate your capacity to handle some of the headaches that come with certain strategies, and to be generally introspective about what’s best for your unique situation.

If you decide that you want to be more hands-off, you may want to consider involving some form of professional property management. Some property managers allow you to have more of a partnership involvement with the property, while others prefer for you to be less involved and just to collect the check.

Of the 5 strategies we’ve discussed, the house hacking and “buy and rent” without a property manager are the most hands-on. Strategies like holding mortgages and buying real estate securities, on the other hand, are much more “hands-off”, though each strategy comes with its own level of risk. “Buy and Rent” with professional property management is somewhere in the middle, but as the real estate portfolio grows more hands-on work is needed to manage the financial and business aspects.

How much capital does it take?

Each different buy and hold strategy comes with its own benefits, risks, and capital requirements. How much you are willing and able to dedicate to your buy and hold investment will affect which strategies best fit your needs as a real estate investor.

More capital-intensive strategies

Mortgage Lending- The most capital-intensive strategy is to hold a mortgage on a property, since you’re acting as the bank for another investor. In some cases, a mortgage holder may be a second mortgage or second lien behind another loan, to help support a purchase. This strategy is more common for the older or more experienced real estate investor who has sufficient capital to lend.

Buy and Rent- It is also capital intensive to buy and rent if you’re not living in the property. As an investor, you need to have the capital for a down payment (typically 25%), cash reserves for the first year of maintenance and capital expenditures, and capital to cover any renovation costs.

Less capital-intensive strategies

House Hacking - One of the less capital-intensive strategies is house-hacking. If you’re investing in multi-family housing (up to 4 units), you can finance with as little as 3.5% down through an FHA loan if you will be living in the property.

With these loans, you typically only have to live in the property for at least one year, and the loan is locked in at the 30-year rate. This contrasts with a pure investment property, where you’re usually required to put 25% down for that same type of property.

Notes in the Secondary Market - The other strategy that we talked about is buying notes, typically in the secondary market. You can buy notes in first or second position, and you can buy performing notes (borrower is keeping current with payments) or non-performing notes (borrower is behind or even on the threat of foreclosure).

While buying real estate notes is a high risk strategy that is only suitable for very experienced investors, it can be less capital-intensive than other strategies. Another benefit from these notes is that you can take possession of the property if foreclosure happens. This frees you up to then switch over to a different strategy with that property, like buy-and-rent.

Real Estate Securities - Investing in real estate securities can also be a great place to start for newer real estate investors or those with less capital up front. Many 401(k) programs offer a real estate fund or target date fund that includes a real estate allocation that allows investors to get exposure to the sector.

What’s the learning curve in real estate investing?

Like any new investment, there’s a learning curve with real estate, especially when larger amounts of capital are involved. Early on, the process can feel slow and uncertain. Finding the right property, building a reliable team, and gaining confidence in your decisions all take time.

As you gain experience, however, that process often becomes more efficient. Relationships strengthen, your ability to evaluate opportunities improves, and decision-making becomes more intuitive.

Sometimes the process can take some trial and error, but if it’s a longer-term goal for you, patience can go a long way. Technology has made the process easier in recent years by making information more accessible and visible to investors.

For investors interested in getting started with a method like house hacking, there’s a concept that is commonly referred to as House Hacking 2.0, where you can generate income from a property you already own. You can do this by taking in roommates, renting out the property on Airbnb for the weekend, or renting out a parking space or storage in your garage, etc.

Investing in real estate securities like REITs, real estate mutual funds, or real estate ETFs can be another easier entryway into real estate for new investors.

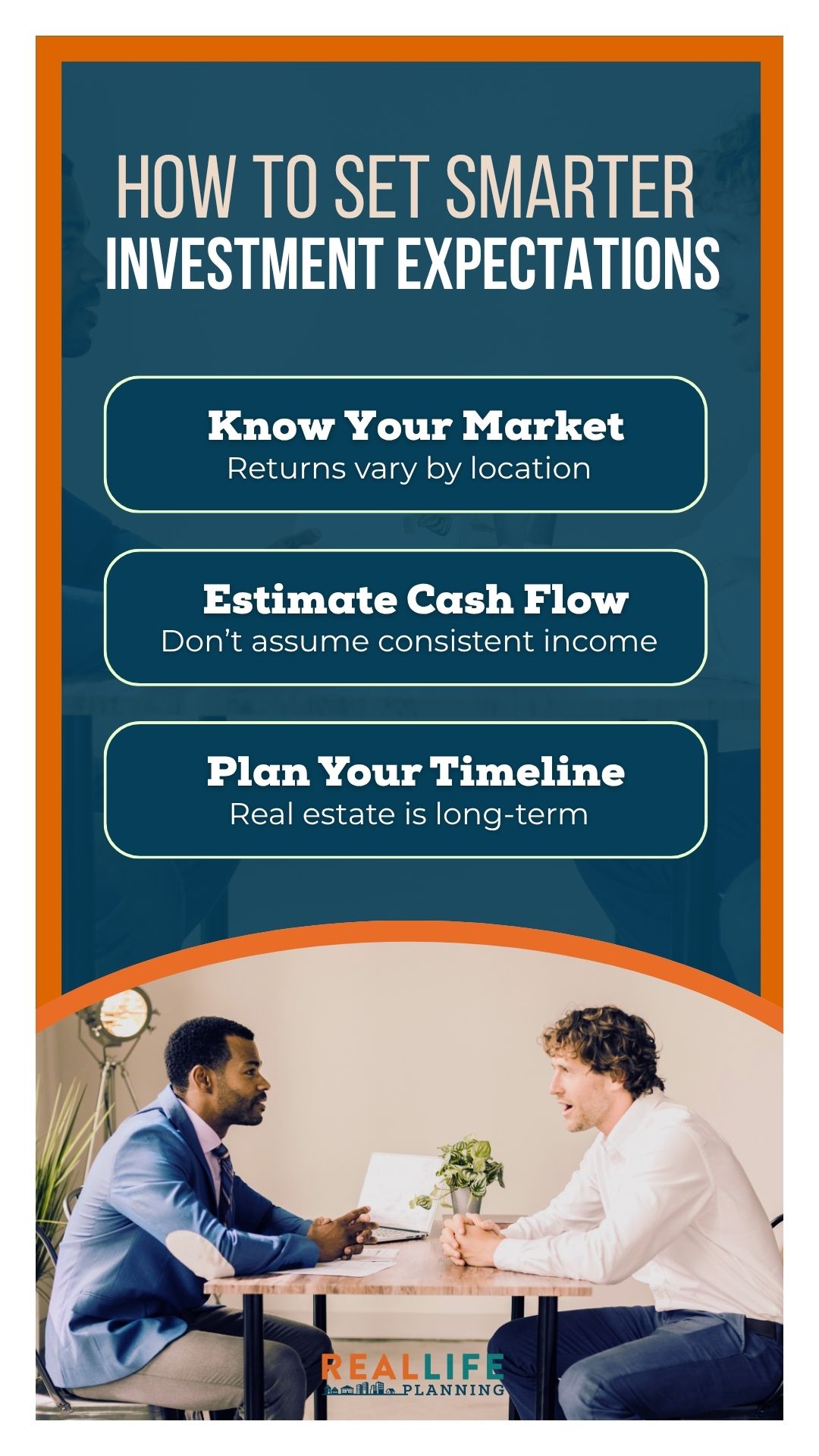

Setting Expectations Around Buy and Hold Investing

Setting Expectations Around Buy and Hold Investing

As a newer real estate investor, it’s important to manage expectations when getting into the sector. Many investors go in expecting steady returns without fully understanding how real estate cycles actually play out.

A general real estate cycle is 18-20 years. If you’re looking to get in and out of an investment in 2-3 years, you’ll likely be leaving money on the table. On the other hand, some investors will say “buy and hold forever”, which may or may not always be the best financial decision.

There’s also a mix of ways that you can make a return on your investment. Considering the neighborhood your property is in, you may make more of your money on cash flow or appreciation. Depending on the mix, you may have to hold the investment for longer to make your targeted return.

Understanding the typical return in the area you’re investing in can help you manage your expectations, and being clear on the estimated cash flow can help you gauge how long you may need to hold the property.

This isn’t to say that real estate investing isn’t worth it; in fact, according to an academic study called The Rate of Return on Everything, housing beat the return on stocks by 16 basis points (or .16 of a percentage point), with a lower standard deviation or volatility than the overall stock market. This is why real estate can be a powerful addition to your portfolio for diversification and returns.

Final Thoughts

“Buy and hold” can be a great strategy for real estate investors, but there are many different strategies that you can get started with, so it’s important to choose the right fit for you. To figure out what’s best for you, you want to make sure you’re asking yourself these 3 questions to start:

- Do you want to be hands-on or hands-off?

- How much capital do you need?

- How easy is it to get started?

These 3 questions are foundational to any decision that you’ll make around buy and hold strategies. Discussing these things with trusted advisors, like your tax advisor, Realtor®, or trusted real estate financial planner, can help you get clearer on what your best path may be.

As with any strategy, there will always be trade-offs. There is no perfect strategy for every investor out there, and understanding where you are in life and your values can help you decide what trade-offs may be worth it for you.

If you have any questions that you'd like to see us talk about regarding financial planning for real estate investors email us at: podcast@reallifeplanning.com

This blog is for general financial education purposes. Information contained in this blog should not be construed as financial, tax, real estate, legal, or investment advice. For educational purposes, blog posts may contain links to other websites which are not under the control or and are not maintained by Real Life Planning. Real Life Planning has provided those links for your convenience but does not necessarily endorse all the material on those sites. Please consult your financial, real estate, legal, or tax advisor for advice specific to your situation.