Financial Planning for House Hacking

Financial Planning Real LifeBy Cynthia Meyer, CFA®, CFP®, ChFC®

What you will get from this article:

| 🏠 | The two main types of house hacking and how to decide which strategy fits your lifestyle |

| 🏠 | How to evaluate the financial benefits and risks of house hacking before diving in |

| 🏠 | What insurance and legal steps to take before renting out part of your home |

| 🏠 | Tax considerations and how to manage mixed-use expenses with confidence |

| 🏠 | Why financial planning is key to making house hacking sustainable and scalable |

House hacking, a method that allows you to make money from a home that you already own to subsidize the cost of owning the property, has been growing in popularity in recent years. It’s a powerful way to get started as a real estate investor, but it can also be a great way to practice multi-generational living or create retirement income.

Though the house hacking strategy has been used for generations, the term “house hacking” was coined by Brandon Turner, one of the original teachers at BiggerPockets. It’s a perfect way to describe the way that investors think about it now — “hacking” your house for additional income.

According to recent research from Zillow, there’s a rising interest in house hacking among younger borrowers. As of November 2023, approx. 51% of Gen Z and 55% of millennials placed a pretty high importance on renting out a portion of their home for rental income while living in the home.

If you asked that same cohort, 56% of Gen Z and 64% of millennial respondents in the survey said that they also placed a high importance on the opportunity to rent out their entire home in the future.

That’s two generations that responded that they look at real estate as a growth asset. Other research from Bankrate and NerdWallet has shown that these types of homebuyers look at their homes as an investment.

That’s why, today, we’re going to break down some of the initial financial planning considerations you want to think about while deciding if you want to get into house hacking.

What Are the Two Types of House Hacking?

There are two primary types of house hacking.

The first is what we like to call “House Hacking 1.0”. This is the traditional house hack, where you buy a multifamily property, living in one unit and renting out the others, or buy a single-family property and renting out space to other people, potentially through an Accessory Dwelling Unit (ADU).

The second type, “House Hacking 2.0”, includes some more creative ways to take this basic concept of using an asset that you live in to create streams of income from it.

Some ways that investors do this are by vacation house hacking (renting out your residence on Airbnb, Evolve, or a similar vacation platform), renting out your garage or parking space, renting out storage space on places like Neighbor.com, renting out your garden for events, etc.

Some people with beautiful homes will even rent them out for photo shoots, parties, or meetings. You can also rent your office (using things like Peerspace) or your pool/part of your outdoor space for travelers. Long story short, there are many ways you can house hack, and investors are always finding new ways to make income from their real estate properties.

What Are the Benefits of House Hacking?

What Are the Benefits of House Hacking?

House hacking comes with many benefits, regardless of how you do it.

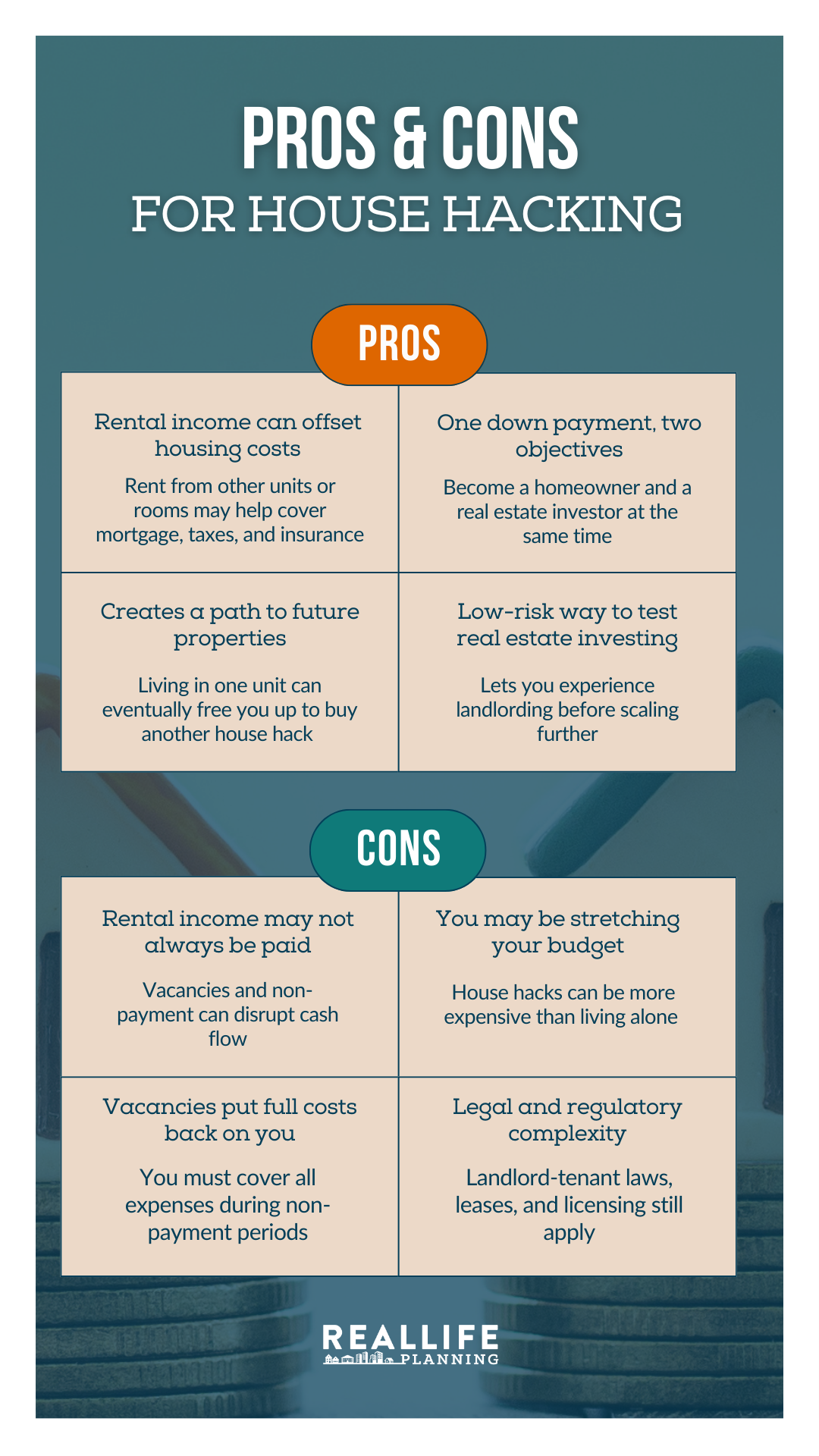

The first benefit is the rental income that you can potentially use to subsidize the ownership of your property, meaning the rent from the other unit(s) covers the cost of owning the property. Many investors move into a duplex, triplex, or fourplex and use the rent from the other units to pay pretty much all of the costs of the mortgage, interest, and taxes on the property.

Another benefit of house hacking is that it can help you get started as a real estate investor and a homeowner at the same time. By using the same amount of capital as the down payment on an investment with two purposes, you can get your foot in the door for both of these opportunities.

Using this strategy, a house hacker may buy a house hack and then eventually move out of their owner's unit to buy another house hack.

Another benefit of the house hacking strategy is that the income from house hacking can be applied to other goals. Investors can use the rental income to help save for a down payment for the next rental property, freeing up additional cash flow in their monthly budget.

House hacking also gives you an opportunity to see if real estate investing is for you. It gives you a preview of what it’s like to be a landlord, so you can decide if it’s something you want to pursue on a broader scale.

What Are the Risks of House Hacking?

As fiduciary financial planners, we want to be sure that you understand the potential risks of house hacking along with the potential benefits.

The first risk that comes with house hacking is vacancies or non-payment. Whether you have tenants in an additional unit or you have roommates in your house or ADU, sometimes they don’t pay, and that income isn’t dependable.

There are landlord-tenant laws that cover how you can handle this type of situation, but there may be long periods of time where you have to cover all of the costs for a property that may be more expensive than you would normally be able to afford if you were living by yourself. This is why it’s very important to practice responsible cash and liquidity management when investing in real estate assets.

The second risk is that the property you plan on using for your house hack may be worth more than you can afford. When you’re considering getting into house hacking, you want to be sure that you aren’t biting off more than you can chew, creating a situation where a non-payment period or vacancy can make it harder to cover all of the expenses on your property.

As an investor, you must also know all of the landlord-tenant laws and short-term rental laws if you’re planning to house hack, the same way you would need to know the laws if you were buying a standalone investment property.

You may need a certificate of occupancy, a landlord license, or a short-term rental license, so you have to know all of the legal guidelines and make sure that you follow them. You also want to make sure your tenants have leases, for example, if you're renting mid-to-long-term.

Insurance Considerations for House Hacking

Insurance is another important consideration when it comes to renting out part of your residence.

If you have a multifamily property, you’ll likely need a policy called Owner-Occupied Dwelling Insurance. If you bought a house and rented to roommates, you’d need a homeowner’s policy. Many house hackers want to have an umbrella liability insurance, as well, to protect them in the case of civil litigation. You may also want to encourage your tenants to have rental insurance.

Before house hacking, you want to make sure you discuss your goals with your insurance agent to get a quote on the appropriate policy to make sure you can cover this expense on top of your other costs.

It’s also worth taking a look at your property from a renter’s perspective and thinking about what could possibly go wrong, to make sure that things like smoke detectors, lighting, fencing, and signs are all in place and working properly to help protect against accidents and mitigate risks.

Short-Term Rental Risks

On top of all of the risks that come with becoming a landlord, short-term rental properties come with their own additional risks, like relatively quick law changes. There could be regulations in your market on short-term rentals; you may or may not need a license, or short-term rentals may not even be allowed in your area.

It’s important to know the rules in your market and understand that these rules could change in an instant.

Tax Considerations for House Hacking

Even if you’ve been DIY-ing your tax returns previously, when you start house hacking, get professional tax advice.

Even if you’ve been DIY-ing your tax returns previously, when you start house hacking, get professional tax advice.

As a real estate owner, you have to take your role seriously. The money that you spend on professional help from a real-estate-savvy tax advisor will be well worth it in the long run, so that you understand your tax situation as you grow and scale your business.

While this is not tax advice, there are some things you want to think about when it comes to understanding your expenses and how that may show up at tax time.

How Are Expenses Treated for Personal and Rental Property?

The first is that the expenses in your house hack are proportionate. Some expenses may be deductible as business expenses, while others may not be, depending on which side of the fence they fall.

For example, if you live in a duplex where each side is exactly the same, and you live in one half while renting out the other side, each side will be treated differently.

On the part of the home that represents your owner's unit in this example, you would take half your property taxes up to the SALT limit on your itemized deductions. You would take half the mortgage interest as well, if you itemize. For half of that unit, the finances of it are going to be treated as if it were your standalone home.

On the other half of the unit, which is your rental property component of the unit, you would deduct 50% of the expenses of the property in this example. This means that you can take half of the property taxes and half the property insurance, which isn't deductible on the personal side.

You can also take half the maintenance expenses for the property as a whole, or any maintenance that specifically applies to that rental unit itself. If you move out of the owner’s unit and rent that unit out, 100% of the expenses then become deductible under your real estate business.

This process can get very complex and complicated, so it’s worth working with a tax professional who is experienced in real estate. For example, to take advantage of things like Section 121 capital gains tax exclusion on the sale of a primary residence, or tax deferred 1031 exchanges, you really need to have a trusted tax advisor on your side to help walk you through the implications and the process.

What Qualifies as Rental Income?

The IRS defines rental income as any payment you receive for the use or occupation of property.

The IRS defines rental income as any payment you receive for the use or occupation of property.

Basically, that means rent from tenants who are in separate units, rent from roommates when you own the house, rent from your midterm tenants, renting out your parking space, renting out storage on your property, renting out the gazebo for a wedding, and these types of situations.

If you rent out your car on Turo, or you rent out an RV that you own and have parked in the yard, or you rent out your boat, etc., that is generally considered business income, not rental income.

For short-term rentals that are seven days or less, where the owner provides substantial hosting services on Airbnb or something similar, that may also be considered business income.

Understanding how to treat these unique situations and the income that you collect is another part of your tax considerations that you want to work with a tax professional to understand.

Final Thoughts

Whatever your situation or unique goals with house hacking, it’s important that you run the numbers and make sure you’re aware of the financial implications of the investment, as well as any regulations and tax consequences.

As real estate financial planners, when clients come to us looking to get into house hacking, we’ll typically run the numbers for the next year and look at the best-case scenario, worst-case scenario, and what the expenses will be to ensure that they can cover the expenses in the case of non-payment or vacancies.

While it comes with many potential risks that need to be planned for, house hacking can be a great tool for those looking to get into real estate investing and homeowning at the same time.

If you’re interested in house hacking and want to see if it’s a strategy that could work for you, we invite you to schedule a call with our team of real estate CERTIFIED FINANCIAL PLANNER™ (CFP®)s to learn more.